Subprime Lending Analytics: Reimagined with AI

- Industry Use Cases

The world of subprime lending is at a crossroads. On one hand, it provides essential credit access to a large and often underserved segment of the population. On the other hand, it’s an industry with elevated risk, where the line between profitability and loss can be razor-thin. For lenders, the challenge is clear: how do you grow your loan portfolio performance and serve your target customers effectively while mitigating the inherent risks of this complex segment? In other words, how do you make risk proof lending decisions?

For too long, the lending analytics has relied on a limited set of tools and metrics for credit risk assessment, with the FICO score being the most prominent. But in today’s economic climate, with increasingly diverse borrower profiles, this one-dimensional view is no longer enough to assess credit risk. It’s time to evaluate the lending analytics approaches. The lenders who will thrive in the coming years are those who can dig deeper, uncovering the subtle, interconnected patterns in their data to gain a proper understanding of their borrower behaviours in the lending process. This is where the power of deep analytics, driven by a new generation of AI, comes into play in subprime lending risk management.

This post will examine the crucial need for in-depth data analytics across the three primary pillars of subprime lending: origination, servicing, and collections. We’ll explore the limitations of traditional approaches and highlight how a new way of thinking about AI-powered data analysis can unlock valuable insights and a sustainable competitive advantage in risk management.

Loan origination is the gateway to your portfolio. Every decision made at this stage has a ripple effect, impacting everything from early payment defaults to long-term financial performance. In the subprime space, the stakes are even higher due to various factors such as limited credit histories and a greater potential for fraud.

The traditional approach to origination analytics often falls short in a few key areas:

Imagine being able to delve beyond surface-level data and ask more nuanced questions. What if you could automatically discover the hidden drivers of credit risk and opportunity in your applicant pool? This is the promise of advanced analytics for better loan performance.

Consider these use cases:

The key to unlocking these insights lies in the ability to explore all possible combinations and permutations of your data automatically. This is where a lending analytics software like dotData Insight changes the game by providing data driven insights for lenders in minutes. By using Statistical AI and machine learning, dotData Insight can connect to your various data sources and automatically engineer thousands of potential “business drivers” – those specific, often non-obvious features that have the most significant impact on your KPIs.

For instance, in the loan origination process, dotData Insight might uncover a driver like: “Applicants with a debt-to-income ratio above X% and who have had more than Y number of address changes in the last Z months.” The platform’s Magic Threshold Discovery would then pinpoint the exact values for X, Y, and Z that are most predictive of loan defaults. This level of granular insight enables financial institutions to transition from a broad-stroke risk assessment to a highly nuanced, data-driven approach to reduce loan defaults.

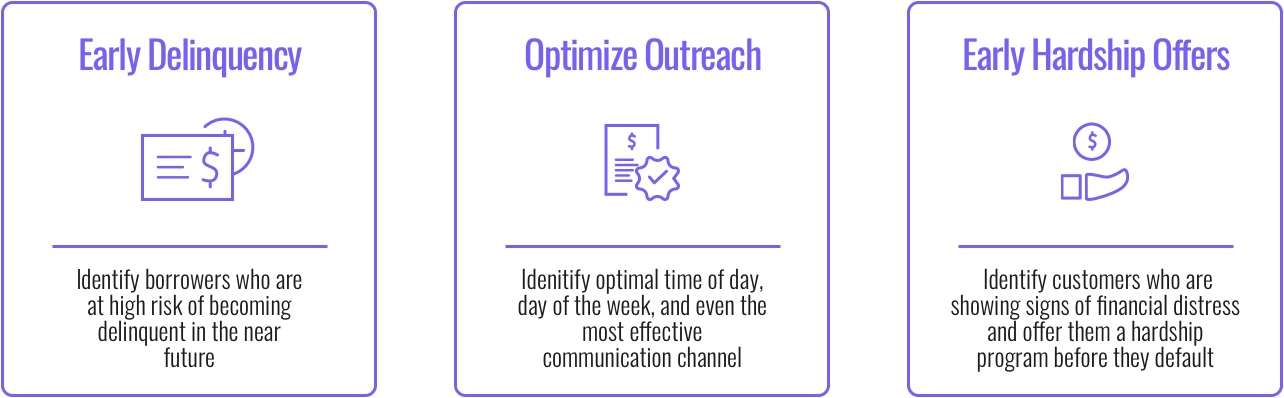

Once a loan is on the books, the focus shifts to loan servicing. This is a critical process that involves everything from collecting payments to ongoing monitoring customer interactions and ensuring regulatory compliance. In the subprime market, where borrowers may experience income volatility, proactive servicing is not just a best practice – it’s a necessity.

Many lenders still approach servicing from a reactive standpoint. They wait for a payment to be missed before taking action. This approach is not only inefficient but can also lead to higher delinquency rates and a poor customer experience.

The challenges with traditional servicing analytics include:

A more advanced approach to servicing analytics focuses on leading indicators and predictive insights. It’s about understanding who is at risk of missing a payment and intervening before it’s too late.

Consider the following use cases:

dotData Insight provides the ability to “stack” these business drivers, allowing lenders to create highly specific micro-segments. For example, an analyst could start with a driver related to payment history, then add a driver about recent call center activity, and then another about changes in bank transaction patterns. As each driver is added, the platform recalculates the impact on the target KPI in real-time. This powerful feature enables lenders to move beyond broad categorizations for borrower’s risk level, such as “high-risk,” and create nuanced segments, like “Borrowers who have made partial payments for the last two months, have not logged into the customer portal recently, and live in an area with a recent spike in unemployment.” Not only providing deeper insights, this is also actionable, transforming servicing from a cost center into a strategic function.

When a loan becomes delinquent, the collections process begins. This is often the most challenging and costly part of the loan management process. The goal is to maximize recoveries while minimizing costs and ensuring a positive, compliant customer experience.

The traditional approach to collections is often a brute-force effort, with agents working through a long list of delinquent accounts. This is not only inefficient but can also be counterproductive.

The key problems with this approach are:

A modern, data-driven approach to collections is all about segmentation and prioritization. It’s about boosting efficiency by focusing your resources on the accounts where they will have the most impact.

Key use cases for deep analytics in collections include:

With dotData Insight, collections teams can move beyond simple age-based segmentation and create sophisticated, multi-dimensional models of recovery likelihood. A business driver in this context might be: “Borrowers who have missed more than three payments in a row, have a low ‘right-party contact’ success rate in the last 30 days, and have a loan secured by a rapidly depreciating asset.” This kind of data-driven insights enables informed decision making on your collection resource allocation, ultimately leading to higher recovery rates and operational efficiency.

The subprime lending industry is not for the faint of heart. However, for those who are willing to adopt a new perspective on data analytics, the opportunities to improve loan performance and reduce risk exposure are immense. The lenders who will succeed in this increasingly competitive market are those who can move beyond the limitations of traditional BI and embrace the power of deep, AI-driven insights.

By leveraging platforms like dotData Insight, you can empower your teams to uncover hidden patterns in your data, understand the “why” behind the numbers, and make faster, smarter data-driven decisions across the entire lending lifecycle. The future of lending is not just about having more data; it’s about gaining deeper and more meaningful insights. And for those who are ready to take the plunge, the future is bright.