Roll Rate Analysis in Auto Lending: Are You Missing Behavioral Risk?

Industry Use Cases

dotData

Join Our Newsletter

Auto lenders face a roll-rate problem that doesn’t always appear on the standard 30/60/90‑day dashboard. On the surface, delinquency curves may look “manageable,” but beneath the surface, accounts are migrating from current to 30, 60, and 90+ days past due faster than they did just a few years ago.

In credit risk management for a subprime lender, captive, or credit union, those numbers indicate a troubling outlook.

In this post, we will look at the challenges of static delinquency views, how they underestimate risk, and how behavioral risk – understanding how payment behavior is changing – can explain roll rate velocity. We will also look at how tools like dotData can perform roll rate analysis and identify the critical drivers that your current models and scorecards may be missing.

Static Delinquency Roll Rates: Necessary, but Backward‑Looking

Lenders still largely manage risk at the end of each period, when they review their portfolios to spot trends and the percentage of balances in each bucket: 30 to 59 days past due, 60 to 89 days past due, and 90+ days past due.

Static delinquency has three strengths:

It is simple, auditable, and widely understood by boards, regulators, financial institutions and funding partners.

It maps into provisioning, Current Expected Credit Losses (CECL), and Asset-Backed Security (ABS) triggers.

It is easy to benchmark against external indices and peer reports.

Static delinquency, however, provides an incomplete picture for some key reasons:

It provides information on how many accounts are already in trouble, not how fast borrowers are moving into deeper delinquency buckets, no early signs.

It does not distinguish between first-time 30-day delinquencies that cure in the next cycle, from a 30-day delinquency that is on a path to a 90+ day charge-off.

It is slow to reflect changes. By the time the 60+ line “blends up,” roll rate velocity has already damaged future loss curves.

In the current economic downturns, where borrowers are stretched by high vehicle prices, longer terms, and layered debt, focusing only on static delinquency roll rates and ignoring its velocity is equivalent to ignoring a leading indicator for your own loss forecasting.

What Roll Rate Velocity Actually Measures

Risk teams and rating agencies have long used transition or migration matrices to understand how loans move between delinquency states over time. Roll rates are simply the elements of those matrices:

The 30→60 roll rate is the share of 30–59 DPD accounts that become 60–89 DPD in the next period.

The 60→90 roll rate is the share of 60–89 that become 90+ in the next period.

The current → 30 roll rate shows early-stage problems before a borrower is classified as delinquent.

Roll rate velocity focuses not just on the level of those transitions, but on how they are changing:

Are 2024 subprime vintages rolling from 30 to 90+ in just two monthly cycles, while 2019 vintages took four?

Historical work on consumer auto portfolios illustrates how powerful this is. An analysis of pre-pandemic data showed that the percentage of 18-29-year-old auto borrowers who moved from 30 and 60 DPD to 90+ DPD nearly doubled from 2014 to 2019, reaching more than 4.1%. These borrowers looked identical in a “static 30-day” bucket view, but behaved very differently in terms of roll rates.

In today’s environment—where overall household delinquency across all debts reached 4.8% of balances in Q4 2025, the highest since 2017, and auto delinquencies are one of the fastest‑rising components—you cannot afford to manage only by the static picture.

Static Delinquency vs Behavioral Risk: Two Different Questions

Static delinquency and behavioral risk answer different questions:

Static delinquency: Did the borrower miss a payment, and how late are they today?

Behavioral risk: How has the borrower’s payment behavior, credit usage, and interaction with you and other lenders changed over time?

Behavioral risk draws on data far richer than a yes/no delinquency flag. Examples include:

Payment timing drift: Does the borrower consistently move from early in the payment cycle to the last days of the grace period, or just beyond the due date?

Auto-pay changes: Did the borrower cancel auto-debit or switch to a manual payment method?

Partial and skipped payments: Has the borrower started making partial payments or is alternating between full and partial payments?

External credit behavior: Is the borrower growing balances on other revolving credit accounts, signaling they might be maxing out credit utilization?

Operational signals: Is the client repeatedly requesting changes to the due date, early extensions, or collection contacts that don’t show yet as a formal delinquency?

Credit-card analytics work has historically shown that the path to a high utilization or delinquency, such as the rapid usage of available credit before cut-off, often has more predictive power than a single utilization report. The same is true for auto lending, where a borrower whose payment date continues to slide for consecutive periods, cancels ACG and opens new lines of personal credit, is a very different risk than a one-off 30-day late borrower who has had temporary income problems, even though they might share the same FICO score and may both be “30 DPD” today.

Static delinquency treats both as identical. Behavioral risk explains why one will likely cure, and the other will accelerate into 60+ and 90+—and why your roll rate velocity is rising even before your static 60+ line moves.

2023–2025 Credit Risk Management: Roll Rates Are Under Structural Pressure

Look at the last three years through a behavioral lens, and the picture gets clearer.

Serious delinquencies are higher: New York Fed reports show that 90+ days delinquent auto loans exceeded 5.2% by Q4 of 2025, up from 4.17% at the end of 2023. The Q4 number was also above the 3.57% long-term average, indicating that the shift was more than just a one-off spike.

Supreme stress: Fitch indices show that subprime borrowers at least 60 days past due reached 6.65% in October 2025, a record high dating back to the 1990s, while prime borrowers remained under 0.4%.

Rising delinquency rates across DPD buckets: VantageScore reports that auto loan delinquencies increased in all days-past-due categories in early and mid-2025, surpassing pre-pandemic levels. In fact, auto lending showed one of the steepest year-over-year increases in early-stage delinquencies.

From a roll‑rate perspective, this tells you three things:

A larger share of borrowers is entering early‑stage delinquency.

Once they enter, more of them transition from one delinquency stage to late‑stage (60–89 and 90+ DPD) rather than curing quickly.

This behavior is heavily concentrated in subprime and younger, lower‑income segments, while prime segments remain relatively stable.

For subprime auto lenders, this pressure shows up as higher 60+ DPD and a growing share of “chronic” 60+ accounts that move between delinquency and cure. For captives, it means weak performance in specific 2023–2024 vintages, even at similar credit tiers, as payment pressure and depreciation interact. For credit unions, rising auto delinquencies are increasingly cited as a top earnings risk and a major concern in regulatory exams, particularly when indirect auto dominates the consumer loan book.

All of that is roll rate velocity in disguise.

Why Traditional Models Are Missing Behavioral Risk

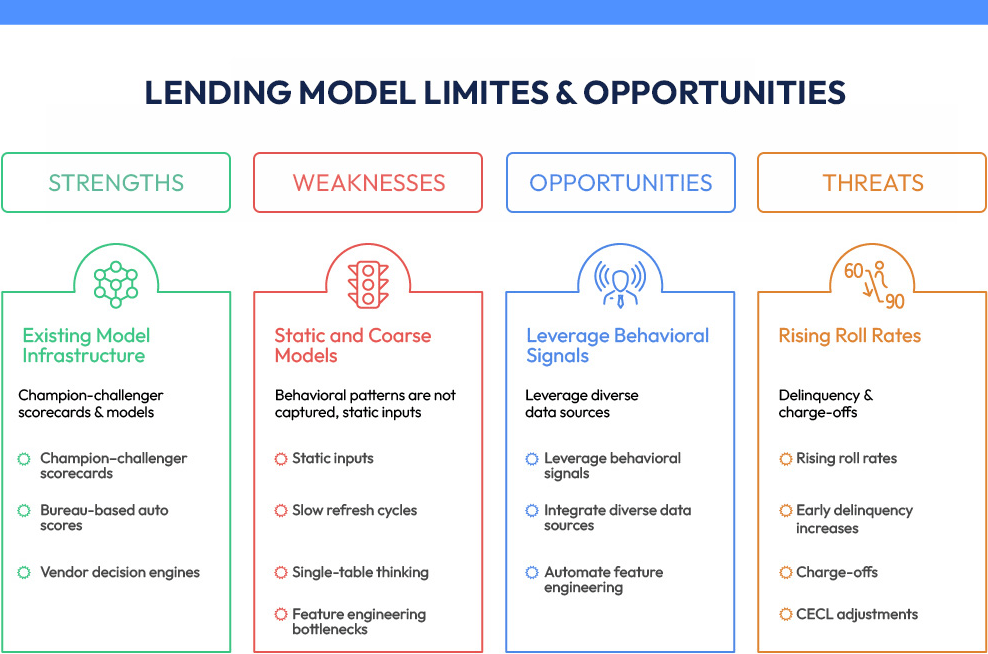

Most lenders did not walk into 2023–2025 unprepared. You already have:

Champion–challenger scorecards.

Bureau‑based auto scores.

Vendor decision engines and application models.

The gap is not that you lack models; it’s that most of those models are static and coarse relative to the behavioral patterns now driving roll rates.

Three practical issues show up again and again:

Static inputs and slow refresh cycles. Scorecards emphasize point‑in‑time variables—current utilization, current DPD status, debt‑to‑income—updated at best monthly. They do not capture sequences of payment dates, autocancel events, or multi‑month trends in “payment‑to‑income stress.”

Single‑table thinking. Many risk teams still work primarily from a single loan performance or servicing table and a bureau extract. Behavioral signals, however, live across applications, dealer feeds, payment histories, bureau tradelines, collections notes, and sometimes customer transaction data.

Feature engineering bottlenecks. Even if your data warehouse contains all those tables, manually building features like “number of due‑date changes in the last six months” or “trend in average days‑past‑due over three cycles” is expensive. Data scientists have to make educated guesses, assemble complex joins, and then repeat that work for each new use case.

The result: most lenders end up with a few hand‑crafted “behavioral flags” and a lot of unexploited signals. Roll rates rise, early delinquency increases, but models still say that risk is “within tolerance”—until charge‑offs and CECL adjustments prove otherwise.

How dotData Helps You See the Behavioral Drivers of Roll Rate Velocity

The good news is that you already have up to date data you need to understand roll rate velocity. The challenge is discovering and operationalizing the right patterns at scale.

dotData tackles that problem in two complementary ways, aligned to the two personas you care about.

For Analytics Leaders and Business Execs: dotData Insight

With dotData Insight, an analytics or BI team starts by defining a KPI table for a specific roll‑rate problem—say, “rolled from 30–59 DPD to 60+ DPD within 60 days” or “every 90+ DPD within 12 months of origination.”

From there, Insight:

Automatically scans data tables—applications, payments, bureau tradelines, dealer and program data, even collections actions—to discover “business drivers” that materially change the KPI.

For each driver, presents:

A plain‑language description of the pattern (for example, “payment posted within last 3 days of grace period in 4 or more of past 6 cycles”).

Prevalence: what percent of historical accounts match the identified pattern?

Lift: How much does the roll-rate KPI change vs. the portfolio baseline in clear percentage or basis-point terms?

Lets you stack drivers to build “micro‑segments”—small slices of the book where the combination of behaviors produces outsized roll‑rate risk or surprisingly strong stability.

For a CRO or Chief Lending Officer, that changes the conversation from:

“Subprime roll rates are up; we should tighten across the board,”

to something like:

“We have a micro-segment of subprime 75+ month term loans with two due-date changes, and recent auto-pay cancellations. These borrowers roll from 30 to 90+ DPD at nearly 2X the portfolio average and represent 0.7% of the portfolio. We can change terms and collections treatment to this micro-segment without punishing the rest of the tier.”

Because each discovered driver is transparent and documented with its prevalence and impact, it’s simple to fold these signals into Post Model Adjustment checks, dealer scorecards, and exam conversations. As a result, lenders can get valuable insights and made informed decisions to prevent potential losses and improve portfolio performance.

For Data Science Teams: dotData Feature Factory

For data science teams, dotData Feature Factory provides the engine needed to discover underlying features across multi-table data without one-off manual engineering efforts.

Instead you:

Define a target table keyed on the entity (loan, account, member) with a target field like “ever 60+ in 12 months” or “ever 90+ DPD.”

Join in all relevant tables—loan performance, payments, applications, dealer metadata, tradelines, work history, etc.

Let Feature Factory automatically generate and evaluate thousands to millions of candidate features, including:

Temporal patterns: Find patterns like rolling averages of “days between due date and payment,” counts of late payments in sliding windows, and payment‑amount volatility.

Cross‑product behavior: Uncover changes in utilization of revolving accounts before delinquency, or the existence of new high‑APR loans.

Dealer and channel context: concentration of certain risk traits by dealer, region, or program.

Feature Factory then ranks features by their contribution to the target, surfacing the behavioral patterns with the strongest lift for roll‑forward risk. The discovered features can feed into any modeling stack, the existing champion-challenger pipeline, internal ML models, or even simple scorecard overlays. Feature Factory maintains the feature pipelines, and SQL code needed for productionization, allowing for:

More accurate roll‑rate and loss‑forecasting models, with better calibration for 2023–2025 vintages.

Tighter CECL and allowance estimates that reflect current behavior, not just legacy patterns.

Granular pricing and line‑management logic measured in meaningful basis points of risk‑adjusted return, rather than broad FICO buckets.

Putting Roll‑Rate Velocity to Work in Subprime, Captives, and Credit Unions

The patterns are similar across segments, but the levers you pull look a little different:

Subprime auto lenders: Start by using behavioral drivers to separate one‑time, likely‑to‑cure 60+ delinquencies from chronic borrowers who drive most of the long‑tail losses. With micro-segments clearly identified, you can:

Tighten dealer and program guidelines in areas with the highest rollover rates.

Trigger proactive outreach when high‑risk payment patterns appear, before accounts hit 60+ DPD.

Measure how even a 50–100 bp reduction in the 60→90+ roll rate translates into lower annualized net loss and lower ABS loss coverage needs.

Captive finance arms: Stack behavioral drivers with OEM, model, incentive, and term patterns to find where certain programs produce faster‑than‑expected migration into 60+ and 90+ despite similar scores. Then:

Adjust term caps, residual assumptions, or dealer tiering for specific micro‑segments rather than cutting entire risk bands.

Feed dealer‑level roll‑rate diagnostics into field management—“these rooftops and programs are underperforming their risk profile.”

Credit unions. Combine behavioral and static views to:

Identify over‑penalized member segments where behavior is stable, but scores are low—candidates for safe growth.

Surface member groups whose payment behavior is deteriorating (later payments, more extensions, strain on other obligations), even if they still look fine by FICO, to protect ROA and exam posture.

In each case, dotData’s role is not to replace your models or decision engines. It is to act as an “AI radar for auto lenders,” continuously scanning your data for hidden risk and profit signals—especially behavioral ones—that your current frameworks miss.

If You Can’t See Velocity, You’re Guessing at Possible Losses

From a distance, the 2023–2025 story is clear: auto loan delinquencies are higher, subprime 60+ DPD has hit record levels, and a significant number of borrowers are progressing into severe delinquency stages across the DPD spectrum.

The question for CROs and data leaders is whether your internal analytics are keeping up.

Static delinquency tells you where you are today.

Behavioral risk and roll rate velocity tell you where you are heading, how fast, and why.

In an environment where a few dozen basis points of improvement in roll‑forward rates can translate into millions in reduced charge‑offs and lower capital strain, treating roll‑rate velocity as a secondary metric is no longer an option. It is the connective tissue between borrower behavior, dealer and program performance, and the loss forecasts that drive your P&L.

dotData Automated Feature Engineering powers our full-cycle data science automation platform to help enterprise organizations accelerate ML and AI projects and deliver more business value by automating the hardest part of the data science and AI process - feature engineering and operationalization. Learn more at dotdata.com, and join us on Twitter and LinkedIn.

dotData's AI Platform

dotData Feature Factory

Boosting ML Accuracy through Feature Discovery

dotData Feature Factory provides data scientists to develop curated features by turning data processing know-how into reusable assets. It enables the discovery of hidden patterns in data through algorithms within a feature space built around data, improving the speed and efficiency of feature discovery while enhancing reusability, reproducibility, collaboration among experts, and the quality and transparency of the process. dotData Feature Factory strengthens all data applications, including machine learning model predictions, data visualization through business intelligence (BI), and marketing automation.

dotData Insight is an innovative data analysis platform designed for business teams to identify high-value hyper-targeted data segments with ease. It provides dotData's hidden patterns through an intuitive, approachable interface. Through the powerful combination of AI-driven data analysis and GenAI, Insight discovers actionable business drivers that impact your most critical key performance indicators (KPIs). This convergence allows business teams to intuitively understand data insights, develop new business ideas, and more effectively plan and execute strategies.