Automated Loan Decisioning: Why Static Scoring Breaks

- Industry Use Cases

The reality for lenders in 2026 is that the choice between speed of execution and mitigating risk has become an increasingly difficult balancing act. Auto dealers demand immediate funding and typically prefer to work with lenders that impose the fewest “stipulations.” Stipulations make loans safer for lenders by requiring the borrower to provide additional verifications – for example, for residency or income. The problem for dealers is that “stips,” as they are known, slow sales cycles. In the simplest terms, more stips mean a greater risk that the sale (and the lender’s funds) will be delayed, stalled, or cancelled altogether if the buyer goes to another dealer. In fact, according to J.D. Power, the speed of funds is the top driver of dealer satisfaction, with dealers significantly more likely to favor lenders that provide funding within 48 hours.

The push for ‘instant funding’ has created a hostile lending environment that pits the human underwriter at a financial institution, who must manually review a pay stub, against a fintech that has likely already funded the deal. While speed is the currency of auto dealers, risk is the killer for lenders. In fact, both auto lenders and credit unions have experienced lower performance on their auto loans, with average annualized losses in subprime auto loan ABS rising to 8.88% in 2025 and 60+ day delinquencies rising to a record high of 6.18%. Even in the credit union space, the delinquency rate for federally insured credit unions was 95 basis points in the third quarter of 2025.

The trade-off between speed and risk, however, is a false dichotomy created by the use of legacy scorecards and outdated manual decision making in the auto lending industry. By leveraging automated pattern discovery, lenders and credit unions can fund more quickly by seeing risk more clearly, moving from manual “stipulation” hunting to validating information using Artificial Intelligence (AI).

Lenders will typically score loans into one of three categories – “queues” – based on a host of data points that are built into their scorecards and ML Models. “Green” queue loans are automatically approved and typically comprise borrowers in the “safe” category with high credit scores and low debt-to-income (DTI) ratios. When a loan application triggers a flag or set of flags (known as “knock out rules”), it sends the application to a red queue and automatically rejects the loan.

The problematic queue is the yellow queue, where the “maybe” applications live. Applications that enter the yellow queue are subject to manual review, often resulting in rejection or abandonment. With most underwriters capable of processing 80 to 120 applications per month, the typical cost of underwriting an auto loan ranges from $40 to $70 per application, excluding document processing, funding, or compliance. Research from Origence shows that moving from manual document processing to an automated lending process can reduce full-time staff requirements from 6.4 to 2.8 full-time equivalents (FTEs). Beyond time and expense, another challenge of the highly manual process in the yellow queue is that human underwriters can be inconsistent, particularly during month-end pushes, leading to errors in income verification and fraud detection.

When viewed in the larger context of annual performance, the numbers become staggering. Consider that subprime specialist Credit Acceptance Corporation reported unit volumes (originations) of 386,126 loans in 2024. If we assume an average cost per processing is $40 per year, a loan originator with similar numbers would incur over $15M in annual costs associated with loan originations.

To address the challenge of the battle between approval speed and credit risk, lenders can turn to the power of automated credit decisioning – and specifically the power of AI by leveraging modern tools that help them identify key signals in tradelines and bureau data that can reduce or even eliminate the need for stips while maintaining or even improving the risk decision profiles. Platforms such as dotData can automatically traverse millions of rows, hundreds of columns, and dozens of financial data sources available to lenders, thereby helping validate a borrower’s claims without requiring physical documentation. The goal is simple, but powerful: move from “condition pending” to “funded” in seconds.

For example, instead of asking for a utility bill to prove residence, a platform like dotData might identify a “Stable Mortgage Tradeline” as a proxy for residence. In this case, AI might determine that mortgage holders have a 99% likelihood of maintaining residential stability, allowing the system to automatically clear the stipulation. Similarly, instead of requiring a pay stub as an income proxy, the system could analyze direct deposit velocity or cash flow consistency, using permissioned access to financial statements and transaction data.

By leveraging AI, lenders can minimize or eliminate the need for stipulations, accelerate loan approval, and reduce human error and risk exposure through a single automated loan approval system. The dealer simply sees an approved application with “Stips: None” and prioritizes the deal. Consortium-based models, on the other hand, flag issues based on broad industry-wide patterns; while useful, they do not enable lenders to leverage proprietary proxies derived from their own portfolio histories, creating a data “moat” that black-box scores cannot match.

An additional element to the battle between risk and speed is the continued erosion of the “safe” borrower. As discussed earlier, traditional lending policies rely heavily on the notion that predefined criteria are indicators of low borrower risk. A potential borrower with a 740 FICO score and a low debt-to-income ratio (DTI) has traditionally been a hallmark of fast loan approval. With average monthly auto finance payments surpassing $750 and routinely extending upwards of 84 months, even traditionally “low-risk” profiles have become increasingly difficult to evaluate properly.

In fact, a 2025 J.D. Power Study shows that nearly one-third of borrowers are now categorized as financially vulnerable. With 29% of new-vehicle purchasers bringing negative equity into the deal, and more than a quarter carrying $10,000 or more in negative equity, the “affordability” of a vehicle purchase is becoming increasingly strained for all buyers. The tri-fold impact of rising automobile prices, negative loan-to-equity ratios, and an inflationary economy has created a bifurcated environment in which borrowers appear sound on paper but are showing signs of stress. In fact, super-prime and prime late payments (90+ days outstanding) have surged 109% year-over-year in the super-prime segment and 47% in the prime segment. Increased reliance on credit cards by as many as 35% of all consumer payments and increases in costs like insurance, utilities, and health insurance that are not calculated as part of DTI all point to a growing number of consumers who “look good” on paper, but are increasingly struggling to make ends meet.

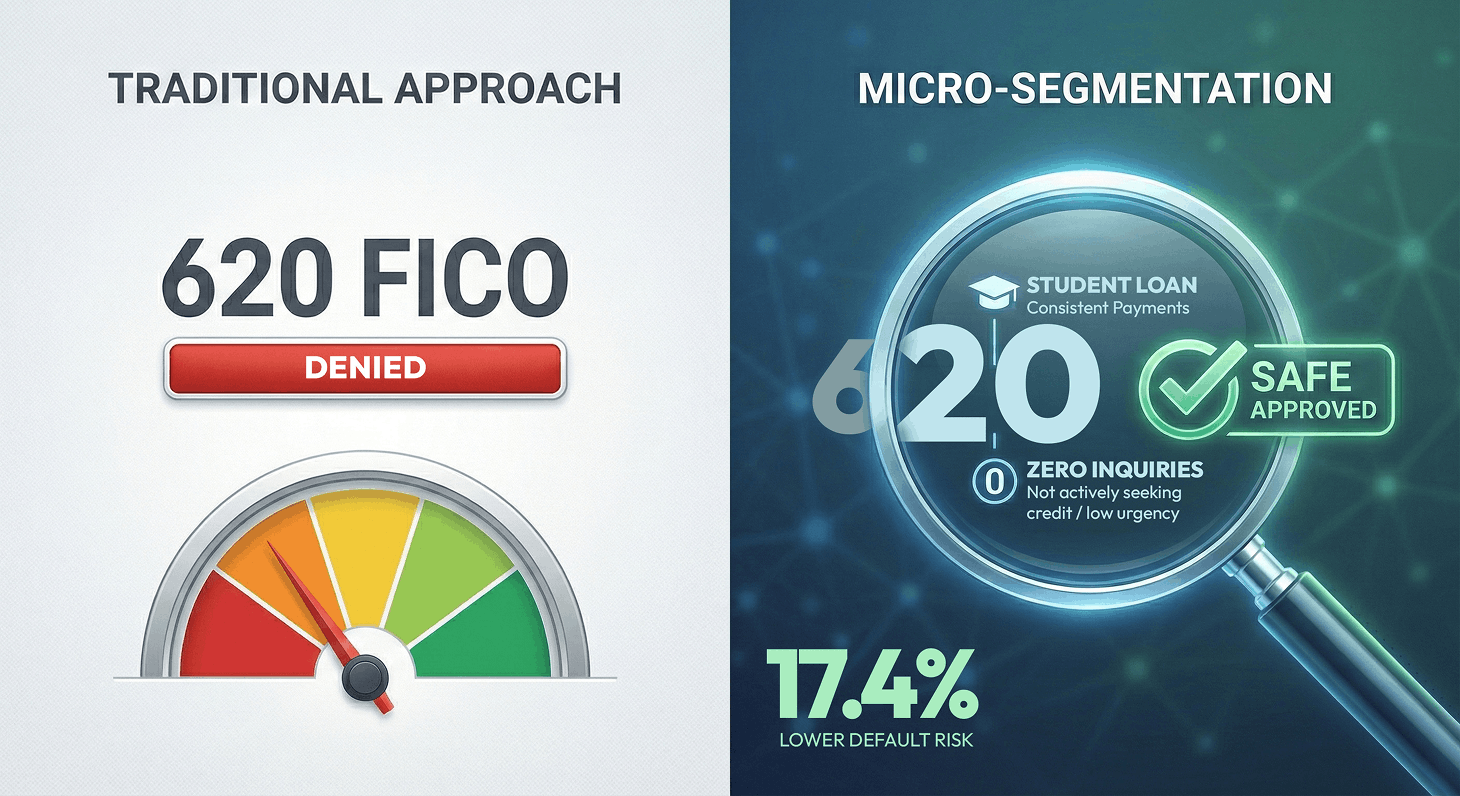

This is where AI-based micro-segmentation can be a valuable tool for lenders and credit unions. Where in a traditional view a borrower with a 740 FICO score and low DTI would be an automatic approval, identifying a small – but high risk – micro-segment of these borrowers who have high velocity of increased credit card utilization in their recent tradelines might trigger a manual review, creating an additional safety net. Similarly, while a traditional approach would flag a consumer with a 620 FICO score as “high risk borrower,” a micro-segmentation analysis might identify that the borrower has an active student loan and no recent inquiries, increasing the likelihood that the borrower is, in fact, far safer than a simple score indicates.

Platforms such as dotData enable both technical and non-technical users to discover and build micro-segments through a process known as “magic thresholding,” which identifies precise statistical ranges to inform critical credit decisions. For example, instead of randomly guessing that “45% DTI is too high,” a lender might find an exact numerical threshold that shows that a DTI > 43.8% triggers a 20% lift in defaults. In this case, the precision of the magic thresholding approach not only increases the pool of viable applicants but also does so without human judgment and with clear, explainable logic.

Removing friction without AI is also not an option. The reason for this is synthetic identity fraud. Synthetic identities have grown by 59% annually since 2020 and by 98% in 2023 alone. With the increasing use of AI, synthetic identity fraud has evolved into a highly industrialized threat, with “Fraud-as-a-Service” enabling bad actors to generate fake identities at scale.

According to Point Predictive, the auto lending industry faces an estimated $9.2 billion in fraud loss exposure for 2025. This represents a historic high, driven largely by income misrepresentation and synthetic identities. Criminal rings use AI to bypass standard Know Your Customer (KYC) checks, and on platforms such as Telegram, “aged” synthetic profiles designed to resemble “thin file” prime borrowers are regularly available.

Standard loan decisioning software is blind to these patterns because it looks for “who the borrower is” rather than “how the data behaves.” Detecting a “washed” credit file requires analyzing features that human underwriters simply cannot find. Just as fraudsters do, lenders must leverage the power of AI to detect signals and nonlinear patterns that are easy to miss, such as a user being rapidly added to other borrowers’ credit card accounts, or signals of “credit washing,” such as disputing valid negative tradelines. This capability ensures that automated decisioning serves as a shield, not merely an accelerator or a means of loan origination.

The challenge of balancing speed and risk in the auto lending industry is, in fact, not insurmountable. Automated Loan Decisioning, supported by transparent artificial intelligence and machine learning, can help lenders aim for frictionless funding with clear risk assessments. “Glass Box” Automation, powered by explainable AI, is the only way to accelerate lending decisioning process while simultaneously mitigating regulatory risk. The ability to audit every decision, demonstrate that proprietary micro-segments are free from human bias, and provide clear, transparent logic behind every approval or rejection is non-negotiable for compliance with fair lending laws and to satisfy examiner scrutiny.

The same technology can also have a significant impact on the P&L of loan originations by reducing the size of the “maybe” queue, where manual underwriting processes increase operational costs and slow loan decision-making. In addition, AI platforms can leverage micro-segmentation and magic thresholding to precisely identify both toxic, high-risk segments and hidden gems that competitors are rejecting. This all leads to revenue growth, loss mitigation, and continuous improvement.

An average increase in a lender’s pull-through rate of 1.8% can translate into an incremental revenue boost of $6.6 million per year. The challenge for auto lenders is to accelerate loan origination decision-making while maintaining a healthy risk profile.

Ultimately, the tension between faster approvals and robust risk mitigation is not a trade-off but a challenge that can be addressed through automated loan processing. By adopting a Glass Box approach, lenders gain the strategic advantage of speed, increased risk precision through micro-segmentation, and regulatory compliance, ensuring a clear path to significant revenue growth and loss prevention.