The Hidden Profit and Risks in Auto Lending Origination

- Industry Use Cases

The U.S. auto lending industry is facing critical stress from record levels of delinquency and $9.2 billion in annual fraud. Legacy risk models are insufficient because they fail to capture unique portfolio signals and actively lose lenders’ money through four key areas:

The solution is to adopt Proactive Signal Discovery using automated Signal Intelligence (e.g., dotData). This approach drives revenue growth by statistically validating hidden stability in applicants, instantly detecting complex fraud patterns, accelerating funding times, and pinpointing/managing systematic risk at the dealer level.

The U.S. auto lending industry is experiencing significant stress, forcing lenders to reevaluate key assumptions about credit risk and loss forecasting. Outstanding auto loan balances surpassed $1.6 trillion in the fourth quarter of 2025, and subprime auto delinquencies hit a record 6.6% early in the year, breaking levels not observed since 1994. Chief Risk Officers, Chief Lending Officers, and VPs of Data Science and Analytics are realizing that legacy models for risk and loss forecasting suffer from critical gaps and miscalculate current consumer behavior. Financial institutions and credit unions can no longer rely solely on models built on broad market data that fail to capture the nuances of each lender’s unique portfolio makeup and do not account for rapidly shifting consumer behaviors and market conditions.

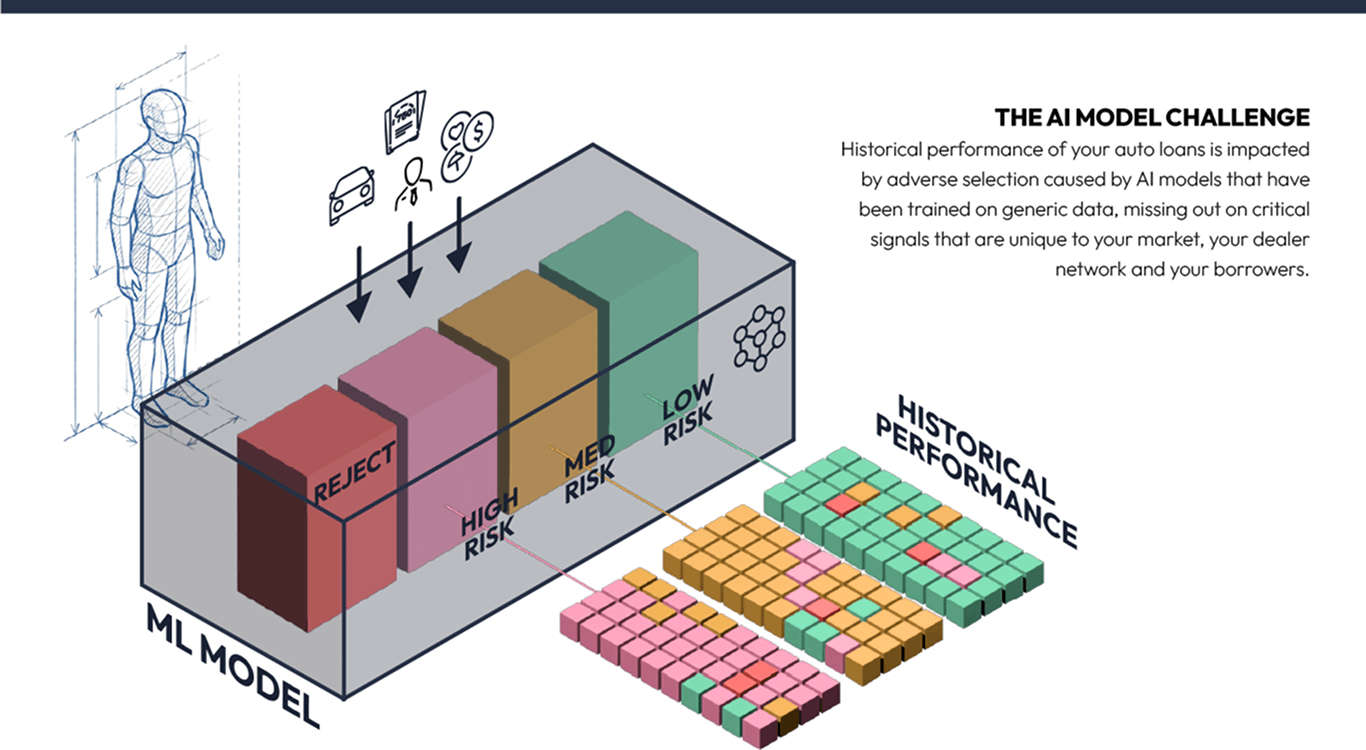

The risk of a consumer defaulting on a personal loan is established the exact moment the loan is booked. A poorly defined approval matrix used in the loan origination process creates a chain reaction of defaults, principal write-offs, and costly vehicle repossessions. Scorecards and out-of-the-box ML and AI models rely on legacy indicators and broad market variables, often accounting for less than 20% of actual consumer behaviors and signals, thereby blinding teams to real-time behavioral shifts and unique consumer and market conditions that each lender faces. Lenders need to recognize that a bad decision at origination triggers a snowballing of risk that becomes visible only when the loan reaches late-stage delinquency.

Evaluating auto loan origination analytics requires leaders to spot vulnerabilities in the lender’s friction within the manual process and warning signals of synthetic adverse selection, where they ultimately win the worst loans in the market. Advanced lending origination software can extract operational signals from complex, structured datasets to perform in-depth analysis of patterns and trends. To find optimal pricing strategies and beat competitors in an ultra-competitive market, lenders must stop looking at isolated data points and begin engineering complex, behavioral signals that expose the hidden realities of their loan applicants.

By definition, most third-party loan origination systems are constrained by their reliance on pooled, heterogeneous data. The sheer volume and complexity of auto lending data possessed by any one lender means generic models must take broad market-wide signals into account, but fail to capture the nuances of an individual lender’s portfolio, the subtle shifts in patterns that are unique to their market or dealer network.

Third-party models can also suffer from “model drift,” in which accuracy degrades as economic and market drivers, such as inflation, vehicle prices, and consumer behavior, change. While advanced ML models allow lenders to incorporate more diverse data, these systems remain fragile unless they are updated continuously to account for “underwater” risks arising from changing used-car prices and rising loan-to-value ratios, a complex and time-consuming process.

Third-party models also force lenders to categorize broad swaths of unconventional borrowers into specific buckets, pushing applicants into or out of the funnel based on broad criteria. The dynamics of this process make adverse selection increasingly likely. When lenders issue rejections based on large, seemingly homogeneous population characteristics, they risk rejecting stable borrowers and sending them to competitors with more precise, narrower scoring criteria. The lenders that are left behind absorb the higher-risk loans and steadily degrade their portfolio performance.

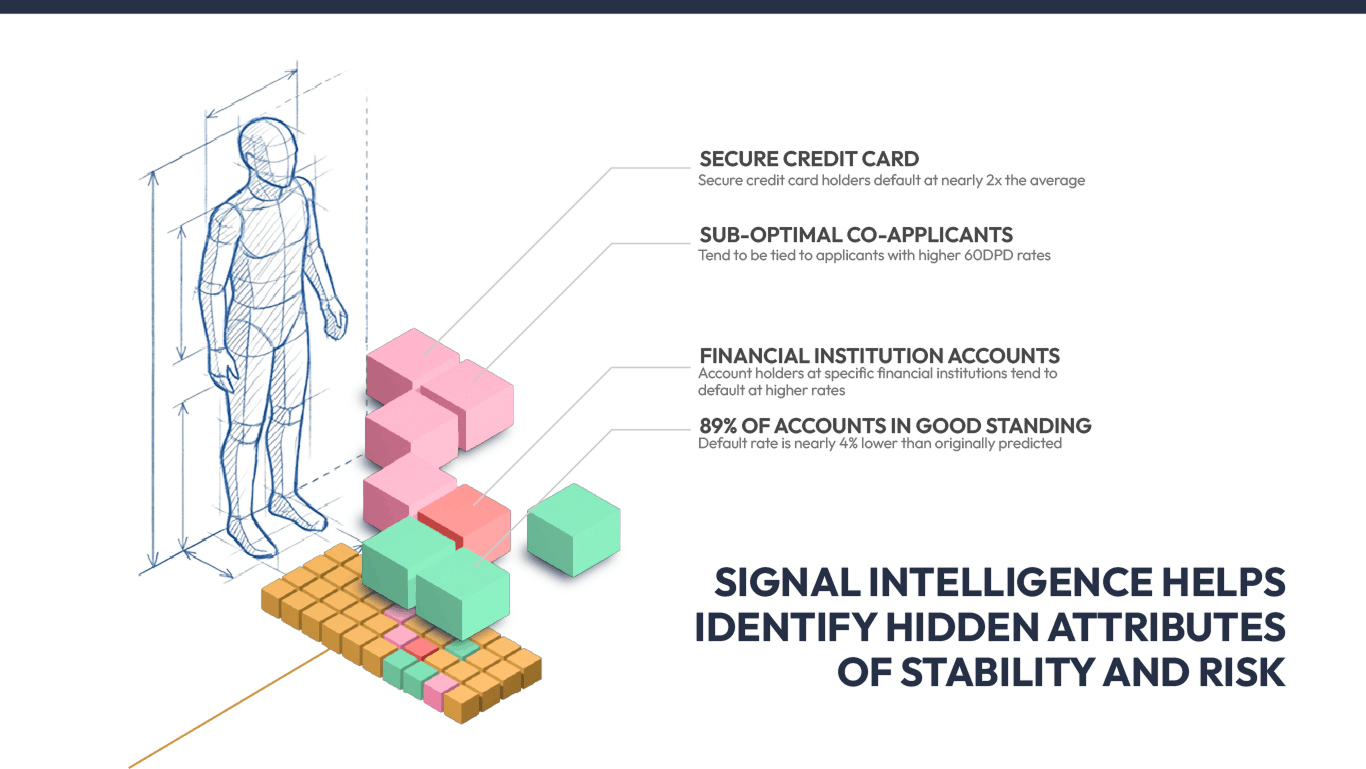

However, when digging deeper into the automatically rejected borrowers, lenders can find sizable micro-populations that actually have stable repayment patterns. Finding the hidden attributes of stability can only be achieved through Signal Intelligence – the programmatic discovery and analysis of complex data sets like transactional cash-flow records or temporal payment gaps. Analyzing the vast volume of data required for Signal Intelligence overwhelms manual underwriting processes and traditional BI and data science tools. Using platforms like dotData Feature Factory, data science teams can bypass tedious manual data aggregation and automatically discover complex patterns hidden in the noise. This automated Signal Intelligence engine identifies nuanced behavioral signals that human analysts often miss, bringing the strongest predictive signals in credit analysis to the top of the leaderboard.

Programmatic signal intelligence isolates the specific behavioral signals that statistically validate an applicant’s creditworthiness. For example, a data scientist can link a target table tracking 90-day delinquencies to associated tables containing Experian tradeline histories and banking transactions. The system evaluates millions of hypotheses to find predictors of success – signals that can be used as Post-Model Adjustments or plugged directly into existing scorecards, providing the empirical proof needed to safely convert an automated “no” into a highly profitable “yes.” By understanding the specific signals that drive performance, data scientists can provide risk committees with the precise evidence needed to approve loans that competitors would reject.

Lenders can increase their funded volume and capture premium yield without altering their fundamental risk appetite. Institutions can find the best pricing strategies and get the most profitable paper in a crowded market by replacing blanket rejections with precision targeting. Lenders can stop giving up yield to competitors and start getting the most out of their auto portfolios by identifying profitable anomalies in pools that appear risky. Every basis point recovered from an incorrectly rejected applicant goes straight to the bottom line, demonstrating that a data-driven origination process is a major driver of revenue growth.

Most auto lenders configure their fraud-prevention systems to scrutinize subprime applicants more closely. Inversely, Super Prime credit tiers can get approved quickly and easily. Organized crime groups exploit this blind spot in lending operations. They create fake identities to circumvent manual income analysis and obtain instant approvals. Fraudsters intentionally target high-trim, luxury vehicles to maximize their illicit yield before vanishing entirely. The financial devastation is highly concentrated, as a single Super Prime synthetic bust-out averages $53,796 in unrecoverable principal.

Auto loan fraud hit $9.2 billion in 2024, up 16.5% from the previous year. These fraud cases keep getting more common—now, out of every 114 auto applications, one uses a fake identity. Among Super Prime accounts with high synthetic risk scores, the late-stage delinquency rate rises to 7.9%. Compare that to the real low-risk borrowers in the same group, and it’s just 0.3%. There’s more: when it comes to delinquent trades with high synthetic risk, the average remaining loan balance is $4,400 higher. Standard skip tracing and repossession methods just don’t work here, since the person on the account was never real in the first place.

Human underwriters just can’t spot the long-term patterns in synthetic identities when they’re stuck with manual tasks of identity verification by checking thousands of data points. Automated Signal Intelligence systems, on the other hand, pick up on mathematical fingerprints—like clusters of inquiries or an unusual surge in newly authorized user accounts. If you feed these engineered signals into dotData Insight, analytics leaders can turn those complicated patterns into dashboards that actually make sense and are useful. Business executives get to understand why a perfect-looking 780 credit score is really just a risky fake, all thanks to the platform’s GenAI-driven data interpretation.

Adding these engineered signals to the decision engine takes away the synthetic fraudster’s main edge. A small drop—just 1%—in false positives at origination saves millions in operating costs and prevents major principal losses. But to really break down the inverted risk pyramid, the analytics setup has to distinguish between real thin-file applicants and fake identities created by criminals. That means digging into things like how quickly credit is being cleaned up and whether someone’s using a Credit Privacy Number. If a profile looks artificially built, the system catches it before the car even leaves the dealership.

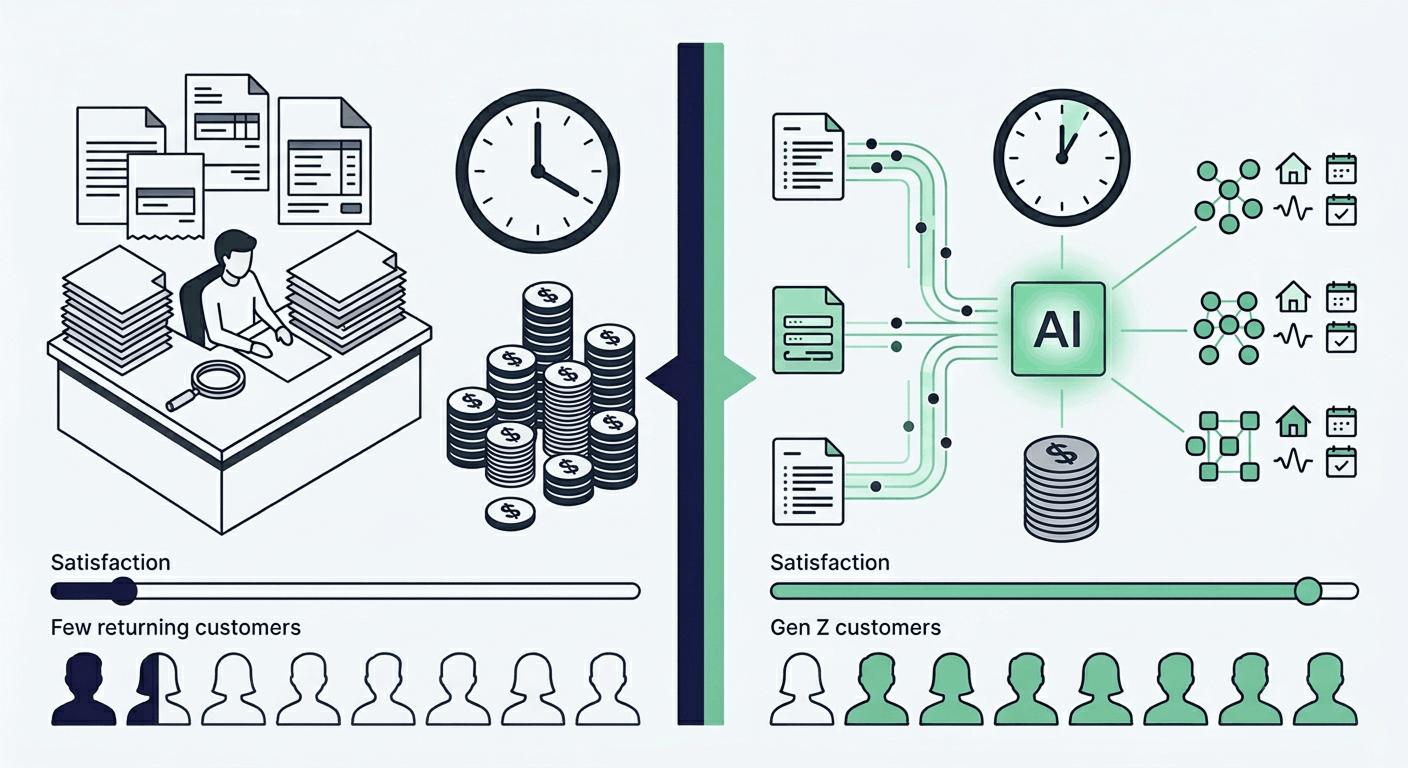

The Book-to-Look-to-Book ratio really matters—it shows the percentage of approved credit applications that actually turn into funded auto loans. Basically, it tells us about operational efficiency, how happy dealers are, and how much friction is slowing things down in the indirect channel. When this ratio drops, it usually means manual checks and paperwork are dragging out the process, so dealerships bail on their approvals and send contracts to lenders who can fund faster. Doing document verification by hand isn’t just slow—it costs lenders $5 to $25 per document and invites major delays and human error. When stipulations pile up, the lender ends up losing the dealer-choice contest right at the point of sale.

Modern consumers and dealer finance offices demand instantaneous execution to finalize transactions. Dealerships will invariably choose the path of least resistance to get a vehicle over the curb. Data indicates that 71% of Gen Z borrowers would return to a lender for future banking needs if they experienced a fast auto loan processing. Relying on manual W-2s, pay stubs, or utility bills creates significant data friction. Risk teams must eliminate this friction without opening the door to income misrepresentation or inflated loan-to-value ratios. Speed and execution reliability directly dictate a lender’s volume and dealer loyalty.

Using dotData Insight, analytics leaders can turn raw bureau data into actionable strategies without requiring advanced coding skills. The platform automatically identifies business drivers that serve as proxies for financial stability and scalable solutions. For example, AI analysis can statistically prove that an active mortgage correlates to a remarkably low probability of default. By stacking these individual business drivers into precise micro-segments, CROs can automatically waive manual stipulations for highly specific borrower profiles. A one-second delay in automated decisioning can redirect a profitable contract to a competitor, underscoring the importance of these lending workflows.

If a borrower meets the criteria of a high-performing micro-segment, the system provides the mathematical justification to bypass manual income verification. This drastically accelerates funding times, lowers the cost of originating each loan, improves operational efficiency, and secures preferred-lender status with dealership partners. Digital lenders effectively replace paper-chasing with data-driven confidence, capturing high-quality loans before competing institutions even finish processing the initial paperwork. Winning the dealer’s choice requires moving at the speed of the modern digital consumer and meeting customer expectations while strictly maintaining the institution’s portfolio risk parameters.

A First Payment Default (FPD) indicates a severe origination failure, rather than sudden consumer misfortune. Industry data reveals that up to 70% of early payment defaults contain explicit evidence of fraud or material misrepresentation on the initial application. First-party fraud—where consumers or dealerships intentionally misrepresent information—accounts for 69% of the $9.2 billion fraud risk exposure facing the industry today. The Early Payment Default Risk Index has increased by 25% over the past 24 months, emphasizing the critical need to track FPD at the dealer level to separate systematic risk from general market volatility.

Systematic risk is frequently introduced by unscrupulous dealer practices, such as utilizing fake employer databases to inflate an applicant’s stated income. Another exceptionally damaging tactic in modern lending is “power booking,” where the dealership’s finance manager inflates the vehicle’s value by claiming nonexistent premium options on the loan application. These practices artificially lower Loan-to-Value ratios and completely bypass the lender’s automated risk controls. Systematic dealer risk can inflate a lender’s default risk for that specific originator by up to 500%.

Risk leaders must evaluate lending analytics at the originator level to pinpoint localized dealer deception. Business intelligence teams can use dotData Insight to continuously monitor FPD rates, roll-rate velocity, and dealer-specific performance deviations. The platform allows users to stack business drivers, for example, by specific dealerships, geographic regions, and early default rates to pinpoint sources of portfolio contamination. By actively monitoring these performance metrics for risk management, lenders can identify which dealerships have added toxic assets to their loan portfolios.

When lenders track dealer performance against set risk thresholds, they can manage dealers with pinpoint accuracy—no need for sweeping policy changes across the whole portfolio that end up hurting trustworthy, top-performing dealers. The Chief Risk Officer obtains hard evidence to confront dealers causing trouble, demand buybacks on fraudulent deals, and shield the company’s balance sheet from organized misrepresentation.

By deploying dotData Feature Factory, data scientists can group application entity IDs by their dealer origin to generate distinct risk signals before losses materialize on the P&L.

Managing a modern auto lending portfolio with static scorecards is simply no longer sufficient for risk assessment. Lenders can’t afford to lose basis points by turning away good borrowers, or by greenlighting fraudsters with applications that slip through the cracks. Lenders need to move beyond legacy methods, reduce manual tasks, and adopt predictive, insight-driven statistical strategies to make informed decisions. Protecting the portfolio starts with spotting borrower risk before a loan ever goes out, which means the risk team has to shift from a cost center to a core part of the portfolio’s health. Executives need to see that portfolio defense isn’t just about running credit checks—it’s about having full visibility into all the underlying data.

Auto lenders need to mine their raw, relational data nonstop to spot hidden signals that give them an edge. When data scientists have access to the dotData Feature Factory Python library, they can automate feature engineering and streamline decision-making. This platform checks millions of hypotheses, surfacing behavioral signals that old-school credit models always miss. At the same time, when CROs and business analysts use dotData Insight, they get a GUI that breaks things down into clear, defensible micro-segments. Every policy change is easy to justify to regulators and makes sense to the board thanks to GenAI interpretations.

When lenders surface these hidden profit and risk signals, they drive down costs, win the indirect channel, and protect their P&L from losses they can actually predict. By blending the raw power of automated Signal Intelligence with business intelligence that actually makes sense, financial institutions steer safely through rough macroeconomic waters. The decision at origination sets the path for the whole company. It’s time to move beyond scorecard limits and embrace the real accuracy that comes with AI-driven signal discovery in making credit decisions.

Legacy models lose lenders’ money through four key areas: 1) Losing profit by rejecting stable, creditworthy applicants (“The Safe NO”). 2) Massive, unrecoverable losses from Synthetic Identity Fraud targeting “Super Prime” accounts. 3) Dealer Friction caused by manual verification, which lowers the Look-to-Book ratio and pushes dealers to competitors. 4) Contamination of the portfolio due to Systematic Dealer Risk, such as “power booking,” which leads to high First Payment Defaults (FPD).

Lenders can recover lost basis points by identifying hidden stability attributes in automatically rejected borrowers using Signal Intelligence. This involves programmatic discovery and analysis of complex data sets to isolate specific borrower behaviors that statistically validate an applicant’s creditworthiness. Every basis point recovered from an incorrectly rejected applicant goes straight to the bottom line.

Organized crime groups intentionally target high-trim, luxury vehicles. The financial devastation from a single Super Prime synthetic bust-out is highly concentrated, with an average unrecoverable principal of $53,796.

A drop in the Look-to-Book ratio, which tracks funded loans against approved applications, usually indicates that manual checks and paperwork are slowing the lending process. Manual document verification is slow, costs lenders $5 to $25 per document, and causes major delays, leading dealerships to send contracts to faster competitors.

Business intelligence teams can use loan origination software such as dotData Insight to continuously monitor FPD (First Payment Default) rates, roll-rate velocity, and dealer-specific performance deviations. By tracking dealer performance against set risk thresholds, the Chief Risk Officer can obtain hard evidence to confront dealers causing systematic risk, demand buybacks on fraudulent deals, and shield the company’s balance sheet. It can serve as a centralized platform with a wide range of integration capabilities to handle loan application intake, streamline processes, and automate workflows, thereby enhancing efficiency.

dotData Insight is an integrated platform where lenders can find everything they need for long-term success in the industry. To learn more about the platform and access additional insights into credit risk, fraud, and loan performance, visit our Lending Microsite, built for lenders.