Early Payment Default in Auto Lending: How Precision Underwriting Stops It Before Funding

- Industry Use Cases

Lenders traditionally rely on fixed credit ratings and tiers, but by adopting Precision Impact Segments, they can block high-risk, mispriced, and toxic loans before funding. Automated systems for signal discovery identify powerful drivers by analyzing data from multiple sources to detect patterns that indicate a higher risk of borrower defaults.

Auto finance institutions are facing new threats as early-stage delinquencies accelerate, leading to growing portfolio losses. According to recent data, total U.S. auto loan debt has breached a record $1.685 trillion. The expansion of debt leaves credit boxes overly exposed, especially since nearly 29% of active auto finance consumers are classified as financially vulnerable to macroeconomic shocks.

Traditional underwriting tools do not capture these vulnerabilities because the analysis is performed on static data points in silos. Deploying dotData Signal Intelligence as a front-end to the analytics process allows credit teams to bypass rigid, rule-based thresholds built on generalized patterns, revealing smaller but highly precise, higher-risk groups. By applying surgical precision to risk tiers, lenders can control the roll rate velocity without restricting overall origination volumes.

Legacy credit decisioning systems struggle to identify income inflation because they are built to evaluate stated borrower attributes as isolated snapshots, rather than variables that change over time. Legacy systems cannot cross-reference multi-table application data with broader dealer performance trends, leaving portfolios exposed to more sophisticated point-of-sale manipulations.

Because dealers optimize their point-of-sale process for financing speed, inflated borrower metrics are sometimes passed to lenders who use static, automated clearance filters to process applications. Relying on such static filters to process unverified applications creates vulnerabilities that traditional scorecards may miss, but adding stipulations to minimize the risk of inflation can slow the lending process and drive dealers toward more automated competitors. The danger is accelerating as new auto loan originations hitting consumers have grown to $182 billion quarterly, giving auto lenders a strong impetus to find new ways to address the challenge.

dotData’s Signal Discovery Console can address this visibility gap by programmatically evaluating relationships between data points across multiple source tables. Risk quants can automatically join tables that contain historical performance data to spot anomalies. By eliminating the need for manual pre-flattening of pipelines, teams can isolate system dealer problems in a matter of hours instead of days or weeks.

Modern credit decisioning systems should be able to discover patterns by combining data from multiple sources to create transparent “Glass Box” business rules. Rules should be easy to combine (or “stack”) and be deployed as post-model adjustments. The platform architecture must deliver clean, explainable parameters that empower risk executives to update underwriting guidelines rapidly without creating technical data backlogs.

Lenders often take on unhedged risks because their technology isn’t fast – or sophisticated enough – to make sense of fragmented, complex data. The operational latency brought on by imprecise decision-making carries penalties, as the auto loan transition velocity into serious 90+ DPD delinquency reached 2.97%. Institutions either play it too safe and lose high-yield volume, or unknowingly book catastrophic defaults.

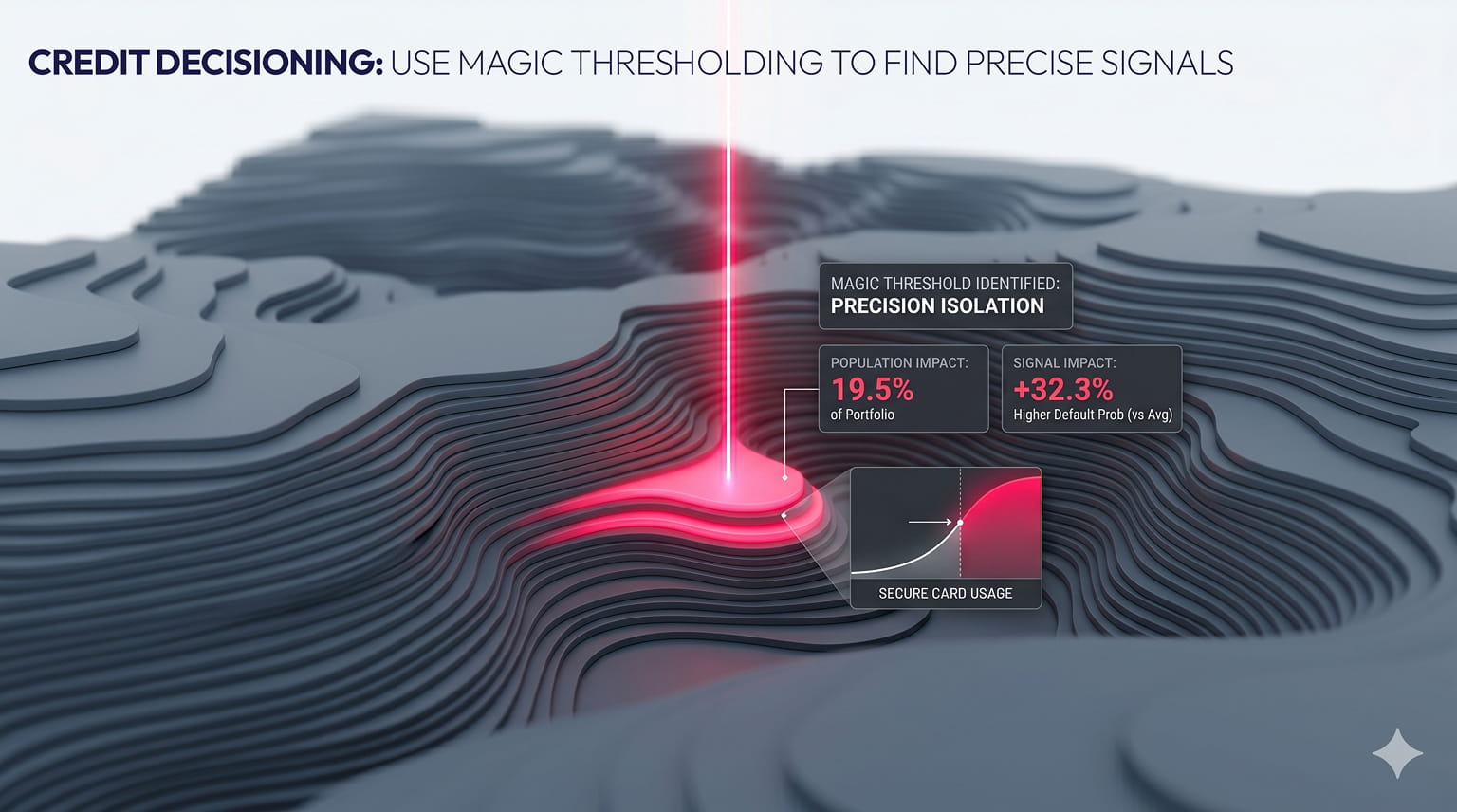

dotData’s Signal Intelligence Workbench shrinks the operational gap by providing a non-technical, point-and-click environment for risk leaders. Through a technique known as Magic Thresholding, users can quickly identify precise high-risk signals without custom programming, enabling managers to combine separate predictors and discover unique predictors that can be deployed quickly.

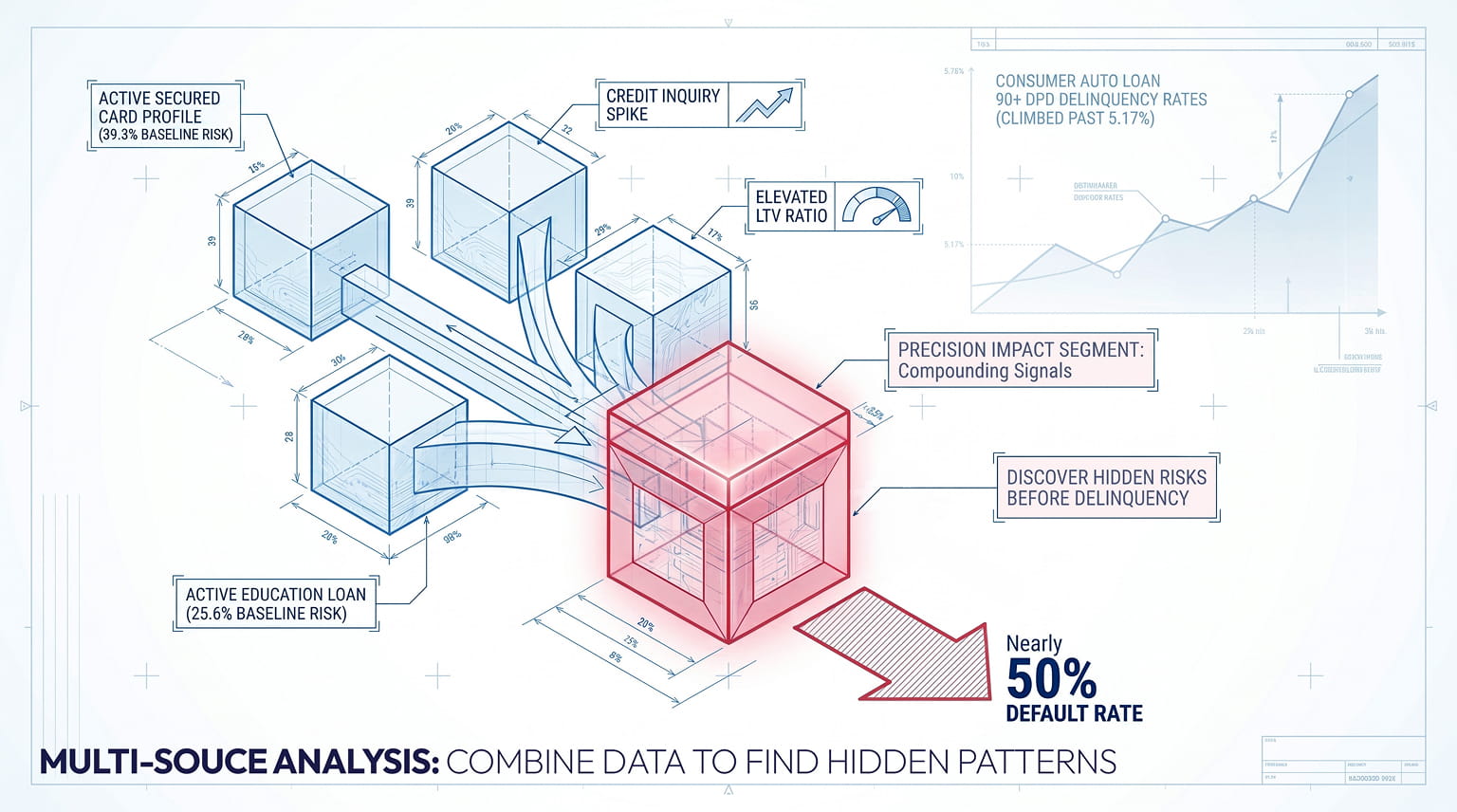

Data models that leverage information from multiple data sources can reduce defaults by automatically combining data from disparate sources into highly predictive customer mini-profiles. Combining data to discover signals allows complex, non-obvious relationships between tradeline behavior and transactions to surface hidden pockets of higher-risk portfolio segments before they become delinquent.

Static credit rules can lead to failure because risk is assessed based on individual attributes rather than on how those attributes change over time and their compounding effects. The blind spot created by looking at static flags in isolation erodes capital reserves as wider consumer auto loan 90+ DPD delinquency rates climbed past 5.17%. A single credit-inquiry spike or an elevated loan-to-value ratio may look manageable until it’s viewed in relation to specific channel behavior.

For example, evaluating an active secured card profile might raise the baseline default risk to 39.3%, while having an active education loan might increase it to 25.6%. Stacking the two signals in dotData would isolate a Precision Impact Segment with a nearly 50% default rate for a very precise pocket of borrowers.

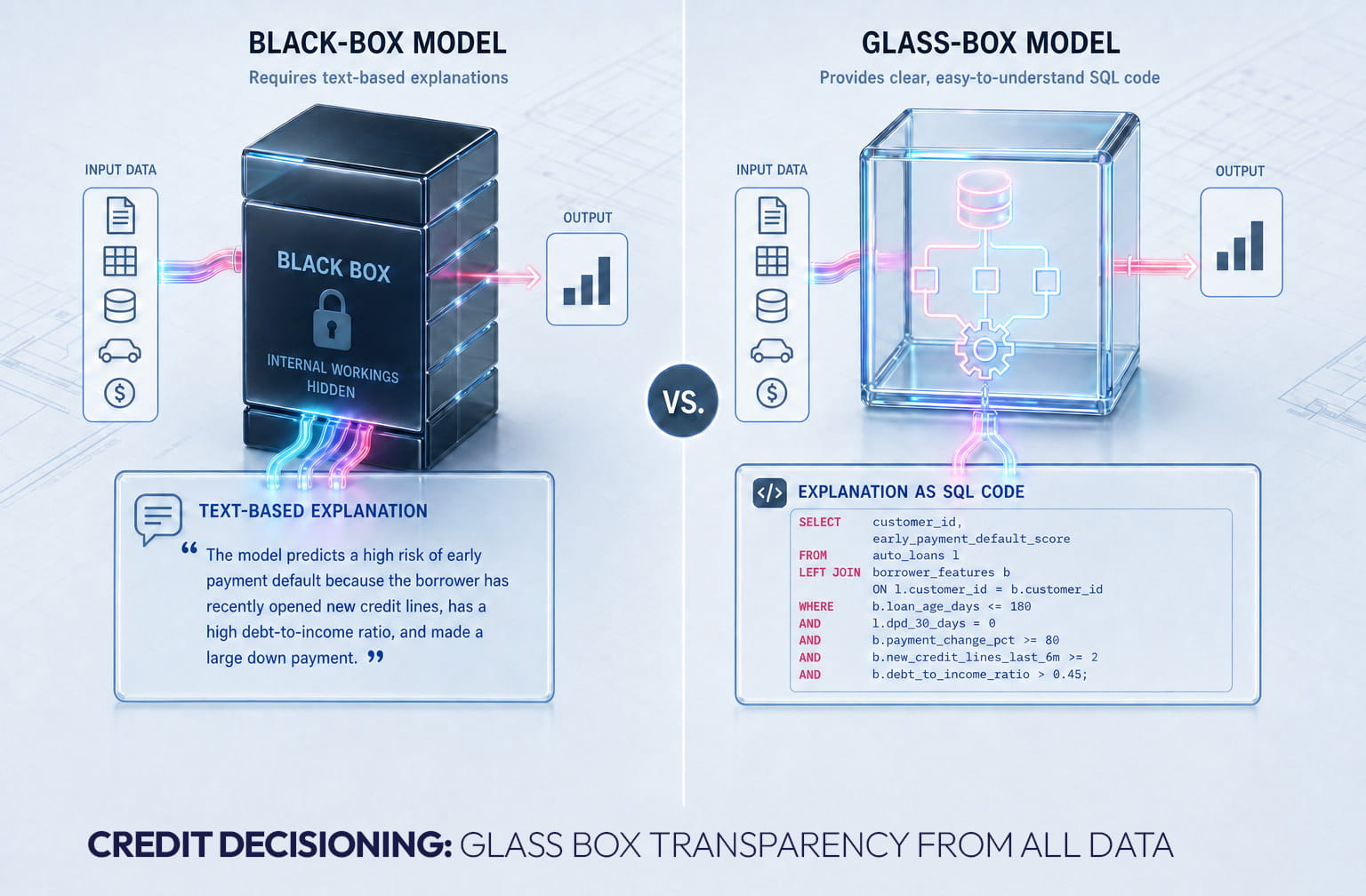

Black-box underwriting engines can affect portfolio performance by obscuring the underlying patterns that drive credit defaults. Black-box AI platforms use conversational text summaries to explain the logic buried within a complex, generic algorithm, rather than outputting deterministic, human-readable rules that allow risk teams to defend policy adjustments easily.

Relying on unadjusted vendor algorithms forces lenders to sacrifice sovereign control over their portfolios during macroeconomic contractions. The danger of this dependency is evident in subprime 60+ days past-due auto loan delinquency indices, which have reached a historic 32-year high of 6.80%. Generic models over-provision capital during downturns, thereby crushing look-to-book ratios without surgically filtering the highest-risk borrowers.

dotData provides an alternative to black-box systems by ensuring transparency is always maintained. dotData generates clear, production-ready SQL rules that can be easily dropped into post-model adjustments in minutes. The inherent transparency provides risk leaders with the precise predictive lift needed to boost the P&L while keeping control over validation protocols.

Through anomaly detection across dealership locations, automated pattern discovery can identify instances and patterns of dealer misrepresentation, giving lenders the flexibility to spot signals of point-of-sale-based income inflation before purchase agreements are funded. By cross-referencing application data, variances in stated assets, bank withdrawal rates, and dealer-specific signals of default, lenders can build strong filters to spot high-risk applications that may require deeper vetting.

Credit unions and captive auto lenders often book large loan volumes from top-performing dealerships, but are frequently unaware of hidden toxic concentrations. Unverified application loops quietly erode portfolio stability, causing sharp spikes in Net Charge-Offs that legacy models often miss. Capturing anomalies hidden in the data requires continuous monitoring of how the data changes across third-party data sources.

dotData performs structural data profiling directly on noisy, unaggregated data, eliminating the need for extensive pre-cleaning. The system automatically ranks the strongest statistical signals and brings high-risk dealer patterns directly to the top of an interactive leaderboard. Through the leaderboard, risk managers can identify risk patterns and factors by combining signals and, in turn, adjust dealer-tier pricing before a negative impact on the balance sheet.

Lenders can reduce early payment default risk by identifying hyper-specific Precision Impact Segments rather than relying on broad credit score tiers. Through automated pattern discovery, risk leaders can identify non-obvious data combinations that flag potential defaults before funding.

Legacy systems fail because they treat application variables as static, flat-file inputs analyzed in isolation. They cannot connect real-time applicant data with multi-table dealer performance metrics and historical payment velocities.

Modern software must provide automated multi-table relational data profiling, transparent business rule generation, and single-tenant, SOC 2 Type II compliant security environments. It requires an intuitive graphical interface for business leaders and command-line flexibility for data scientists.

Multi-source, multi-table models combine records from the Loan Origination System, the Loan Management System, and external data sources, including credit bureaus and other third-party providers. By combining data from multiple sources, hidden compounding risk signals can be discovered that traditional single-table scorecards and models ignore.

Black-box models can create systemic portfolio blind spots because they summarize risk using conversational text overrides rather than transparent signals. The lack of granularity means risk leaders are unable to adjust pricing with the surgical precision needed to prevent harm to application pull-through rates when broad, sweeping changes are made.

Automated pattern discovery leverages Artificial Intelligence and Machine Learning across multiple dealerships to identify and analyze concentrations of anomalies in applications. The platform automatically ranks these signals via an interactive leaderboard, allowing credit unions and lenders to intercept inflated assets before loans are booked on the funding date.