Why Aging Reports Can Drive Auto Loan Charge-Off

- Industry Use Cases

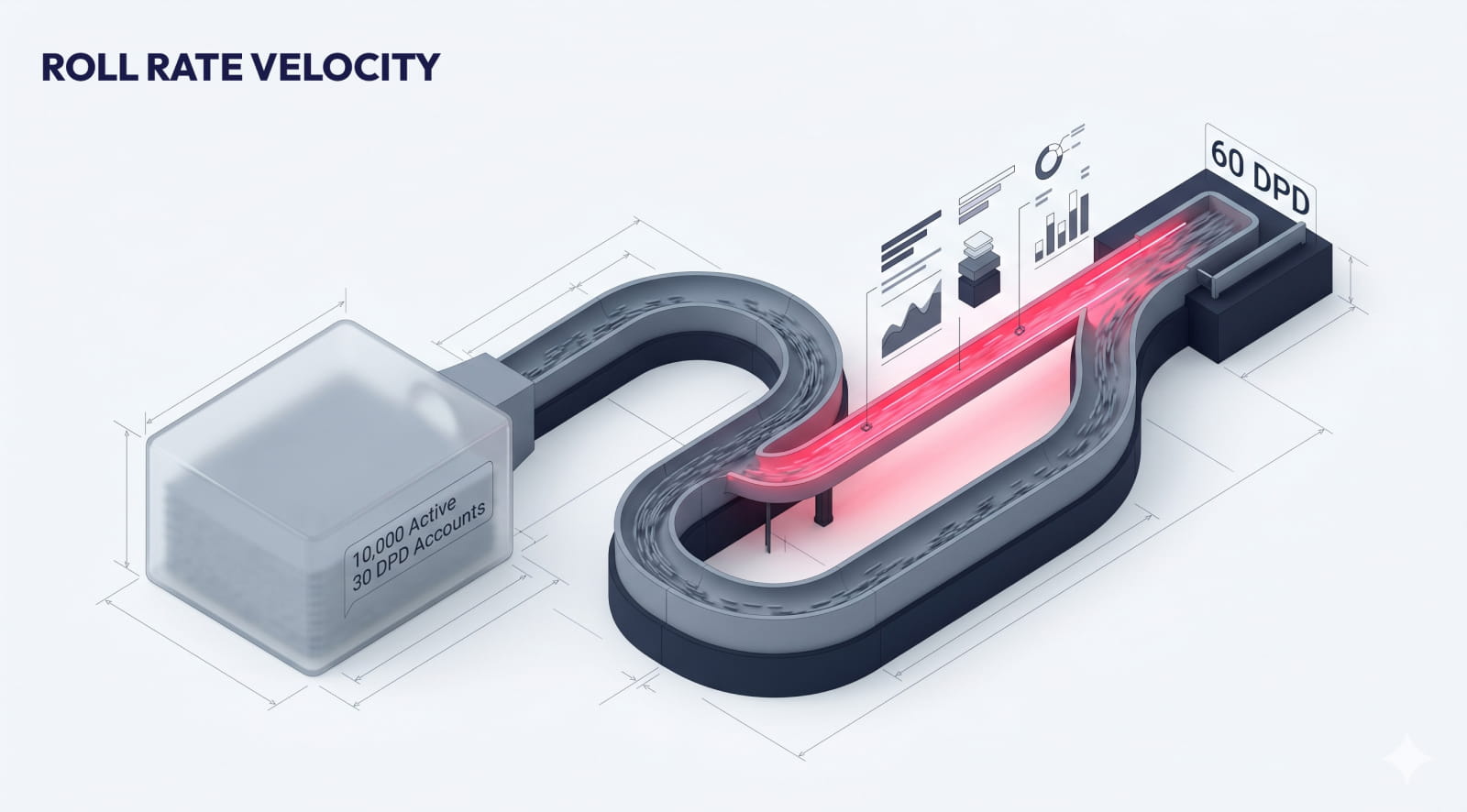

Roll rate velocity measures the speed at which accounts move between delinquency stages. Especially important is the transition from 30 to 60 DPD. Monitoring roll rate velocity identifies the acceleration of risk before moving to charged-off accounts, providing the only viable window for effective intervention.

Many Chief Risk Officers rely on outdated information. By the time a loan reaches 60-DPD, the likelihood of bringing it current (known as “curing” the loan) has decreased. Lender or collection agency often starts manual outreach when borrowers reach 60 days, using aging reports. The practice highlights a key challenge in traditional credit performance, as it relies on broad strokes of information that is often outdated.

The auto lending industry is seeing significant shifts, with subprime 60-day auto delinquencies reaching 6.80% in late 2025 and 90+ day delinquencies growing to 5.21%. With increasing delinquency rates, roll rate velocity becomes the primary tool for distinguishing borrowers who will ultimately become current from those headed towards default.

Monitoring the transition from 30 to 60 DPD can provide key insights into negative trends. In a portfolio with 10,000 active 30 DPD accounts, a 5ppt increase in roll rate from 25% to 30% means that 500 additional accounts, worth millions in value, have moved toward a likely loss. Signal Intelligence can detect these shifts at the dealer and regional levels, allowing detailed adjustments to provisioning.

For executives, tools such as a Signal Intelligence Workbench provide front-end visibility into the movement of accounts from 30 to 60 DPD. A tool like the Signal Discovery Console can also provide back-end support for data scientists by automatically identifying behavioral triggers that precede a roll. This dual-layer approach keeps the strategy ahead of emerging risks.

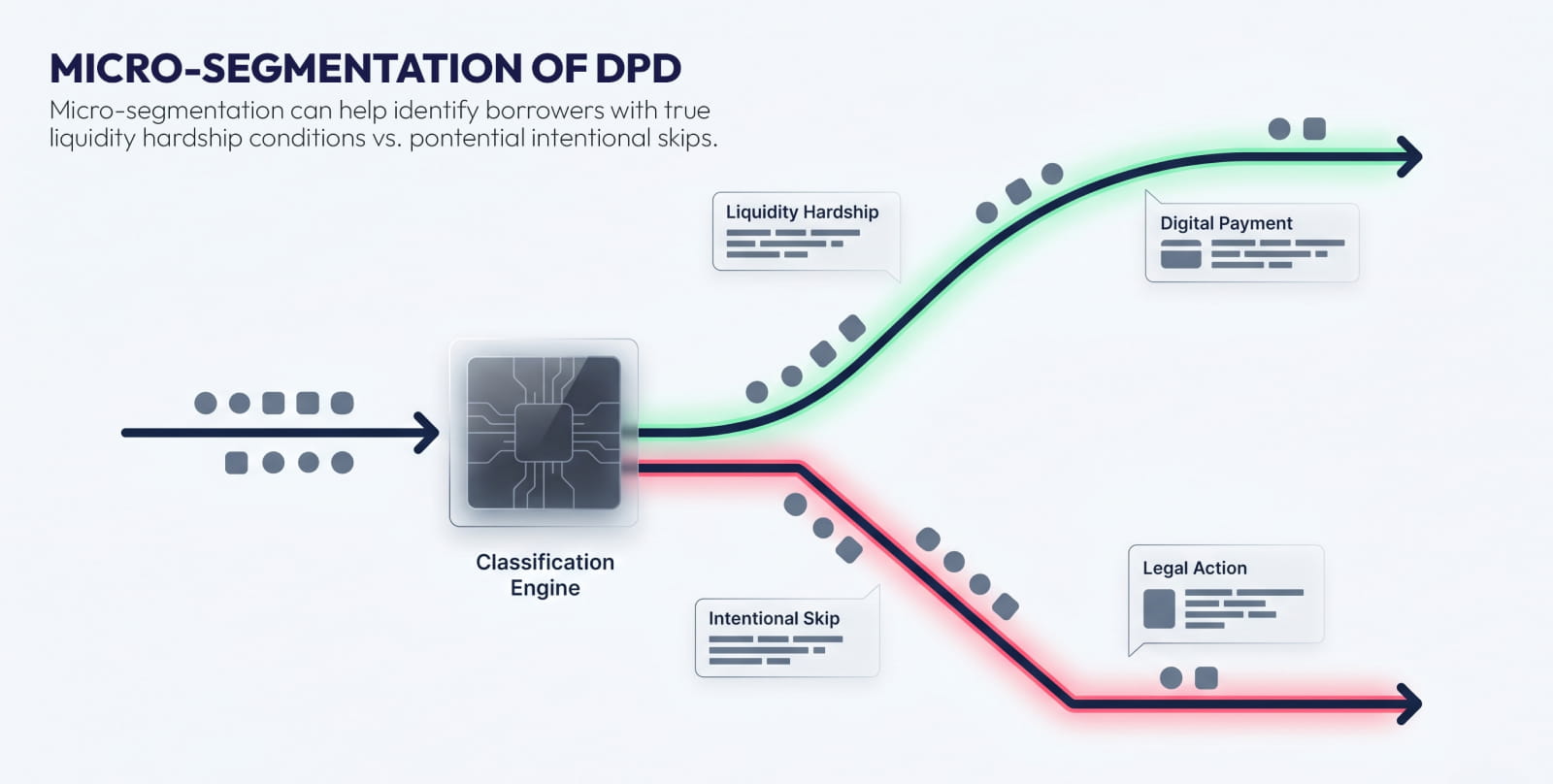

An Intentional Skip is a default where a borrower deliberately hides the vehicle to avoid repossession. Unlike a “liquidity hardship,” in which a borrower lacks funds but is willing to cooperate, the intentional skip requires immediate tracing and legal action to attempt recovery, rather than a traditional collection script.

A growing number of borrowers took out unsecured car loans with no intention of fulfilling their monthly payment obligations. These strategic defaulters use synthetic identities or exploit negative equity to move vehicles across state lines. According to industry reports, auto loan fraud reached $9.2 billion in 2024, a 16.5% year-over-year increase.

The problem is also not unique to subprime auto loans. The NCUA quarterly summary shows that net charge-off ratios for credit union auto loans had increased significantly by late 2024. Traditional debt collector call scripts fail because they assume the borrower is likely to be cooperative and is dealing with missed payments only due to a temporary cash-flow problem. In reality, recovery teams are often chasing unresponsive accounts that have no intention of becoming current, while repossession completion rates have dropped to 27%.

A major global auto manufacturer identified a high-risk micro-segment by analyzing accounts with more than 50 collection calls and negative roll momentum. The identified group had a 54% loss rate, showing significant potential savings by moving these accounts directly to skip tracing. Signal Intelligence flags these micro-segments for immediate skip tracing instead of standard phone outreach.

Data latency occurs when building and deploying risk models takes longer than the time for a delinquent loan to become a car loan charge-off. Manual feature engineering, which typically takes 6-8 weeks, forces lenders to analyze accounts that have already reached the point of no return.

Data science teams often face an overwhelming volume of raw transaction logs and a multitude of related datasets that are often unexplored. When model development takes two months, the resulting analysis no longer reflects the borrower’s current behavior. In non-prime lending, this delay is comparable to managing risk with outdated information.

A leading subprime auto lender realized that using traditional techniques for identifying new risk signals was slow and time-consuming. The tedious nature of the process meant the company relied on lagging indicators, such as FICO scores, and on outdated AI models that had not been updated in over 12 months. The challenge was that manually discovering new signals consumed nearly 95% of the analysts’ time due to data complexity and volume, leaving the team missing opportunities to detect previously missed risk signals.

Motorq research found that the success rate of repossessions is declining as the time required to recover vehicles increases, underscoring the cost of delays. Signal Intelligence identifies dozens of risk patterns in hours, compared to the weeks it takes with traditional techniques. A signal discovery engine can scan relationships across multiple data tables to identify payment gap signals that traditional scoring models miss.

Signal Intelligence can identify “Bad Actor” dealers by uncovering upstream origination patterns that correlate with short-term delinquencies. Signal Intelligence can detect where dealers manipulate trade-in values or waive “Proof of Income” to bypass approval engines and secure funding for high-risk borrowers.

Unscrupulous dealers can fool the loan approval process by overpaying for trade-ins to hide a lack of a down payment, baking a potential default into the loan before the transaction is even complete. NCUA state-level reports have noted the impact of inflated LTV ratios on portfolio health.

With tools like a risk strategy workbench, credit leaders can quickly surface dealer-specific micro-segments to identify activities more likely to be associated with higher-risk dealers. Building micro-segments can provide a precise way to target only dealers more likely to issue problematic loan requests, protecting ROA without disrupting the entire dealer network, unlike broad policy changes.

Cost Per Dollar Collected (CPDC) is optimized by identifying and reallocating resources away from “self-cure” accounts toward high-risk “intentional skips.” This requires Cure Rate Optimization to ensure that expensive human collectors are not calling borrowers who would have paid anyway.

The collection floor is a lender’s highest overhead. Calling every 15-DPD account with the same intensity simply means burning through margin on clients who are likely to become current on their own, so-called “self-curers,” while ignoring 30-DPD borrowers that are statistically likely to roll to 60-DPD. Signal Intelligence can provide Payment Propensity Score (PPS) modeling that includes behavioral data.

Industry benchmarks show that the cost per dollar collected can decrease from $0.22 to $0.12 by using AI-powered technology. Operational costs can also drop by 40% to 60% when routine borrower interactions are automated. Shifting from a volume-based approach to one that prioritizes clients based on clear signals can completely change the scope of the recovery process.

The use of advanced AI technologies can improve recovery rates by 10%. Identifying borrowers who are more likely to self-cure enables lenders to use digital options for making payments instead of costly proactive outreach campaigns. The targeted reallocation of resources is key to protecting margins in a high-delinquency market.

Roll Rate Analysis is measured as the percentage of accounts that move from one delinquency bucket to the next one over a fixed period. Roll-rate velocity tracks individual accounts across buckets over consecutive months to predict losses.

Involuntary repossessions have several costs that quickly add up, including skip tracing ($50-$200), agent visits ($100-$300), and towing ($200-$500). When combined with forwarder fees, total costs can reach up to $1,000.

An affordability problem is driving the current surge, driven by record-high vehicle prices, interest rates often over 14% on used cars, and inflation-adjusted wages that have not kept pace with the rising cost of living.

Lenders can reduce CPDC by using tools like Signal Intelligence to build micro-segments to identify and stop calling “self-curers.” Properly segmenting lower-risk borrowers reallocates resources to high-risk accounts, dropping operational costs by 40-60%.

An Intentional Skip is a planned default in which a borrower deliberately hides collateral and ceases all communication. These cases often involve synthetic identities or credit washing and have significantly higher loss rates.